.gif)

%20(1)%201.png)

Building the Fintech Dream

The Latest Content

Most Canadian marketplace operators know exactly how much work it takes to build a merchant network worth being part of. Years of onboarding, relationship management, traffic building and problem solving on both sides of the transaction, all of it stacked up to create something that genuinely works.

Then a customer reaches the payment screen and leaves because the option they were looking for simply was not there. The merchant never finds out why, the cart sits abandoned and neither of you can trace the problem back to a checkout that was not built around how Canadians actually prefer to pay.

Canadians tap on the go, move money directly from their bank account via Interac and increasingly expect to complete an online purchase without a card anywhere in the process. The Interac payment gateway they rely on for rent, bills and everyday spending is the same infrastructure they are looking for when they land on your merchants' checkout screens, and most Canadian marketplace platforms are simply not giving it to them.

Online payment processing Canada in 2026 is not a space where card-only checkout is a defensible position anymore, and the operators who have not addressed this are absorbing the cost through merchant churn they cannot quite put their finger on.

Why Canadian Marketplace Checkout Has Become a Competitive Differentiator?

The Canadian marketplace space is more crowded in 2026 than it has ever been. The Canadian e-commerce market is projected to grow at 9.6% annually, pulling more platforms, more operators and more merchants into an environment where the differences between platforms are getting harder to articulate on product alone. Commission structures, onboarding speed and category breadth were once enough to distinguish one marketplace from another. In 2026, the most decisive differentiator has moved somewhere most operators were not watching closely enough, which is, the merchant checkout Canada experience their platform delivers to end customers.

Merchants evaluate platforms with a sharper eye on what their customers will experience at the payment step, because their own revenue depends on it. A merchant losing sales to checkout abandonment on one platform is not going to stay quiet and hope next month improves. They look at what payment methods for Canadian merchants other competing platforms are offering, and they make decisions accordingly.

The Canada payment gateway market is currently valued at USD 2.68 billion and growing at 22.75% annually, which reflects just how much operator and merchant attention is now following the checkout conversation. For merchant acquiring businesses in Canada managing networks of sub-merchants, getting checkout right has stopped being a technical afterthought and started being the reason merchants choose one platform over another.

What Payment Methods for Canadian Merchants Actually Look Like in 2026?

Understanding what your merchants need at checkout starts with understanding what their customers are actually doing at the payment step, and the picture in Canada in 2026 is specific enough to act on.

Canadians have strong, established preferences around how they move money, and those preferences do not soften when they land on a marketplace checkout. 58% of Canadians trust Interac e-Transfer over PayPal, and 52% say they are as comfortable paying a small business via Interac. These are not marginal preferences. They represent the mainstream of how Canadian consumers think about digital payments, and they belong to the customers your merchants are trying to convert every day.

The payment methods for Canadian merchants that actually reflect this reality in 2026 go well beyond a standard card field. Canadians want options that feel familiar and low-friction, bank-direct payments via Interac, mobile wallets for on-the-go purchases and payment flows that do not require them to reach for a card they may not want to use for that particular transaction. The gap between that expectation and what most marketplace checkouts deliver is wide enough to be measurable in abandonment rates, with 43% of Canadians willing to abandon a cart entirely when their preferred method is not available.

For marketplace operators, this is not a consumer behaviour trend to monitor at a distance. It is the standard your merchants are being held to by their customers right now, and the platforms that help their merchants accept Interac payments Canada-wide are the ones giving those merchants a genuinely competitive checkout experience rather than a limitation they have to work around.

The Checkout Mistakes Canadian Marketplace Operators Keep Making

Most of these are not dramatic failures. They are quiet gaps that accumulate over time and become expensive to diagnose once they are embedded in how the platform operates.

Offering card-only checkout and calling it done

Cards cover a portion of Canadian customers but leave out a genuinely significant segment who prefer to pay directly from their bank. When those customers land on a merchant's page within your platform and find only a card field, the sale is over before the merchant knows it was ever in play.

No fallback when a payment method is unavailable

A checkout that offers one payment method and nothing else has no recovery path when that method does not work for a particular customer. The customer does not wait around to figure out an alternative, and the merchant absorbs a lost sale they will likely never trace back to the payment screen.

Assuming Interac means a separate integration per merchant

This is arguably the most common misconception among operators managing larger networks. The belief that enabling bank-direct payment options for merchants Canada-wide requires repeating a complex technical process for every sub-merchant is what keeps many platforms stuck on card-only long after they know it is costing them.

Inconsistent checkout experience across the merchant network

When different merchants on the same platform offer different payment options because the platform has no unified sub merchant payments Canada infrastructure, the customer experience becomes unpredictable. That unpredictability erodes the trust that a marketplace brand depends on across its entire network.

Not connecting checkout gaps to merchant churn

Merchants attribute slow months to product issues, pricing or traffic. The operators managing them often do the same. Checkout abandonment caused by limited payment methods for Canadian merchants rarely gets named as the source of the problem, which means it simply does not get fixed.

What Poor Checkout Costs Merchants on Your Platform?

There are costs here that go beyond the abandoned transaction, and they tend to surface in ways that are genuinely difficult for merchants to diagnose from inside their own data.

Cash flow delays that compound at volume

Card settlements run on a T+1 to T+3 cycle. For merchants doing meaningful volume, that gap between transaction and settlement is a consistent cash flow constraint they are carrying every single week. Bank-direct payment options resolve this at the source rather than at the accounting level.

Fee structures that quietly erode margins

Merchants on your platform are absorbing card processing fees on every transaction, and on already thin retail margins that percentage adds up faster than most merchants track it until they sit down and do the annual calculation. Within a merchant acquiring Canada network, sub-merchants often have limited ability to negotiate better rates independently, so the platform's payment infrastructure becomes their cost reality.

Chargebacks that cost far more than the original sale

A disputed card transaction costs the merchant the sale, the product if it has already shipped, a processor dispute fee and the internal time spent building a response. For merchants operating within a marketplace without strong merchant payment solutions Canada infrastructure behind them, managing that process efficiently is genuinely difficult. Bank-direct payments eliminate this category of loss entirely because those transactions are irrevocable.

A reputation problem they did not create

When checkout feels limited or unfamiliar, customers associate that friction with the merchant they were buying from rather than the platform behind the payment screen. A sub merchant payments Canada infrastructure problem at the platform level quietly becomes a review problem at the merchant level.

Conversion gaps they can see but cannot explain

Merchants who list on multiple platforms compare performance across them. When one platform consistently delivers weaker numbers at the payment step, merchants notice. The connection between limited payment options and lower conversion is rarely named explicitly, but it shapes how merchants think about where they put their effort.

What Strong Merchant Payment Solutions in Canada Look Like?

Getting this right in 2026 is less about adding every possible payment method and more about offering the ones that actually match how Canadian customers manage money, consistently, across every merchant on the platform.

For a Canadian marketplace, strong merchant payment solutions Canada means the checkout experience your merchants deliver is not dependent on what each individual merchant has been able to set up independently. It means the platform carries the payment infrastructure, and every merchant on it benefits from that without needing to negotiate their own processor relationships or manage separate integrations.

In practical terms, what that looks like is a checkout that includes bank-direct payment through a reliable Interac payment gateway alongside existing card options, accessible through a single API connection at the platform level. The ability to integrate Interac e-Transfer API at the platform level means operators are not repeating a complex technical process for every sub-merchant they bring on. One integration extends to the entire network, and every new merchant that joins inherits a checkout that already works for Canadian customers.

Here is how card-only checkout compares to a multi-method checkout built around what Canadian customers actually use:

A merchant payment gateway Canada that handles this at the platform level is not just a checkout upgrade. It is a structural advantage that compounds as the merchant network grows, because every new merchant joins a platform that already gives their customers what they are looking for at the payment step.

The Marketplace Platforms That Get Checkout Right Will Pull Ahead

Canadian marketplace operators who solve this now are not just fixing a current problem. They are building a payment experience that compounds in their favour as their merchant network grows, because every new merchant that joins inherits a checkout that already works for Canadian customers rather than one they have to compensate for.

The operators who wait tend to find that merchant churn and conversion gaps are considerably more expensive to reverse than they were to prevent. Merchant payment solutions Canada infrastructure built at the platform level scales with the network, and the gap between platforms that have it and those that do not will become harder to close as the market normalises around better checkout standards.

FlexMerchants, built by FlexM, a leading global fintech conglomerate, equips master merchants to add Interac to checkout across their entire network through a single API integration, giving every merchant on the platform a payment experience that matches how Canadian customers actually want to pay.

1:1 session to explore checkout options tailor-made for Canadian marketplaces.

.png)

How confident are you that your business could survive a POCAMLA audit, if the Financial Reporting Centre requested your records this week?

POCAMLA Kenya has governed how businesses handle customer identification, due diligence, and suspicious activity reporting since 2009, but the Act enforced today looks nothing like the one written back then. It has been amended multiple times since, most significantly through the 2025 Amendment Act, and each round has brought tighter obligations while pulling in businesses that were never covered before.

That evolution is exactly why so many compliance teams get caught off guard. A policy built around an older version of the law, or around what felt sufficient a few years ago, rarely matches what POCAMLA Kenya actually requires now. Most businesses still treat AML compliance Kenya as something they set up once and revisit only when a problem forces them to, and that habit is precisely what the current version of the Act was written to catch.

What Is POCAMLA?

POCAMLA Kenya, formally the Proceeds of Crime and Anti-Money Laundering Act, criminalises money laundering in Kenya and sets out what businesses must do to stop their services being used to move illicit money. It became law in 2009, but the version enforced today is far stricter than the one originally written, shaped by several rounds of amendment and most recently by the 2025 Amendment Act, which raised penalties sharply and brought many more businesses under its scope.

Beyond the Act itself, a set of detailed regulations spells out how it works in practice. These cover how customer identity gets verified, when a transaction needs to be reported, and how long records must be kept. Anyone still working off an older understanding of POCAMLA Act Kenya is likely missing changes that now shape what compliance actually looks like.

POCAMLA Requirements Kenya: Who Must Comply

POCAMLA organises reporting institutions into two categories, and neither carries lighter obligations than the other, regardless of how differently they operate day to day.

Financial institutions cover the businesses most people associate with AML law in the first place:

- Banks and microfinance institutions

- Insurance companies

- Capital markets firms and stockbrokers

- Money remittance and payment service providers

- SACCOs

Designated Non-Financial Businesses and Professions, or DNFBPs, is the second category, and it has long included:

- Lawyers and accountants

- Casinos, both land based and online

- Dealers in precious metals and stones

Real estate agencies are the newest addition to this list, formally brought under the DNFBP definition, with the Estate Agents Registration Board now empowered for AML oversight. Many agencies that never considered themselves part of a regulated sector now carry the same due diligence and reporting obligations as a bank.

Industry labels have little bearing on whether POCAMLA requirements Kenya apply to a given business. What matters is exposure. Any entity handling client funds, facilitating high value transactions, or operating close to how wealth changes hands sits within scope, whether it has historically thought of itself as regulated or not.

Financial Reporting Centre Kenya (FRC): Registration and Supervision

Every reporting institution's relationship with POCAMLA runs through one body, the Financial Reporting Centre Kenya, which functions as the country's financial intelligence unit. Registration with the FRC isn't optional or informal. It happens through a dedicated online portal called goAML, and it's the first real signal to the regulator that a business understands it falls within scope and is prepared to operate accordingly.

Once registered, the relationship doesn't end there. The FRC expects reporting institutions to submit an annual compliance report by the 31st of January each year, detailing how the business has met its obligations under POCAMLA and the supporting regulations over the preceding twelve months.

Supervision itself is sector based, meaning the FRC works alongside regulators specific to each industry, the Central Bank of Kenya for banks, the Capital Markets Authority for capital markets firms, and the Gambling Regulatory Authority for casinos, while retaining overall authority to request records, investigate gaps, and take action where something doesn't add up. For a business that treats registration as a one time formality rather than an ongoing relationship, that's usually where the trouble starts.

Core POCAMLA Compliance Obligations

POCAMLA compliance in Kenya is not a single task completed during onboarding. It is a chain of obligations that runs for as long as a customer relationship exists, and each link in that chain sets up the next.

Customer due diligence and enhanced due diligence

Every reporting institution in Kenya has to verify who its customers are and assess the risk they carry. Standard due diligence covers most customers, but enhanced due diligence Kenya rules apply where the risk is higher, including:

- Politically exposed persons and their close associates

- Customers linked to high risk or FATF grey listed jurisdictions

- High value transactions

- Customers with complex or unclear ownership structures

Suspicious and cash transaction reporting

Once a business identifies risk, Kenyan law requires that risk to be escalated formally.

- A suspicious transaction report Kenya (STR) must reach the Financial Reporting Centre once suspicious activity is flagged, and under the 2025 Amendment Act, delaying that report is treated as non-compliance in its own right.

- Cash transactions carry a separate reporting duty. A cash transaction report Kenya (CTR) is required for any cash transaction equivalent to or exceeding USD 15,000, filed through goAML, regardless of whether the transaction itself appears suspicious.

Ultimate beneficial ownership

Reporting institutions in Kenya are also required to look past the individual in front of them and identify who ultimately owns, controls, or benefits from that customer, particularly where a company or legal structure is involved. Beneficial ownership Kenya POCAMLA requirements have tightened considerably in recent years, closing what used to be a common gap in corporate onboarding.

Record keeping

None of the above holds up without documented proof it happened. POCAMLA record keeping obligations, set out under Regulation 37 of the Proceeds of Crime and Anti-Money Laundering Regulations, require customer identification records, due diligence notes, and transaction records to stay accurate, complete, and retrievable, with a minimum retention period of seven years.

Each obligation looks procedural on its own. Lined up together, they form the exact sequence an FRC inspection tests, and the gaps that surface are usually the ones where one step in that chain was treated as optional.

POCAMLA Penalties for Non-Compliance

The financial risk of getting POCAMLA wrong is steeper than most businesses expect, and it isn't a single flat number. Under the Proceeds of Crime and Anti-Money Laundering Act, POCAMLA penalties scale with both the offence and the entity involved.

- Up to 14 years imprisonment for an individual convicted of money laundering, alongside a fine of up to KES 5 million or the value of the property involved, whichever is higher

- Up to KES 25 million, or the value of the property involved, whichever is higher, for a company convicted of the same offence

- Up to 50 percent of the amount involved as a separate penalty for failing to declare monetary instruments crossing Kenya's borders

- An additional KES 10,000 per day for continued non-compliance, capped at 180 days

A business that assumes one number covers every scenario is usually underestimating what it's actually exposed to, especially once cross-border transactions enter the picture.

Kenya's FATF Grey List Status in 2026

Kenya was placed on the FATF grey list in February 2024, and it remains there as of the June 2026 plenary. Algeria and Namibia both exited that same review cycle after demonstrating sustained reform, a contrast that makes Kenya's continued listing harder to treat as a formality still working itself out in the background.

The practical consequences are already visible across how Kenyan institutions do business internationally:

- Correspondent banks apply heavier scrutiny to cross-border payments routed through Kenyan institutions

- International partners lean more heavily on enhanced due diligence before entering new relationships

- Investors factor grey list exposure directly into risk pricing before committing capital

- Approvals that once moved quickly now come with additional documentation requests, or in some cases, don't come through at all

This exposure attaches to the jurisdiction, not to any single institution's individual track record. Every business operating under Kenya FATF grey list 2026 conditions absorbs a share of that scrutiny by default, regardless of how disciplined its own compliance programme happens to be.

POCAMLA Compliance Checklist

Understanding the obligations is one thing. Proving them in practice, on demand, is what actually holds up during an FRC inspection. Most gaps trace back to one of the following being treated as settled once and never revisited since.

- Registered with the Financial Reporting Centre through the goAML portal

- Documented AML/CFT policy in place, covering onboarding, CDD, and escalation procedures

- Risk-based customer due diligence process applied consistently across all customers

- Enhanced due diligence triggers clearly defined for PEPs, high-risk jurisdictions, and complex ownership structures

- Beneficial ownership identification built into onboarding for corporate and legal entity customers

- Suspicious transaction reporting process that can move quickly once risk is flagged

- Cash transaction reporting process in place for transactions at or above the USD 15,000 threshold

- Records retained for a minimum of seven years, in a format that's accurate, complete, and retrievable on request

- Staff trained on AML obligations relevant to their role, rather than a generic annual refresher

- Annual compliance report submitted to the FRC by the 31st of January deadline

The businesses that hold up under scrutiny aren't the ones with the most polished policy document. They're the ones that can produce evidence against every line above without needing a week to prepare for it.

Staying Ahead of POCAMLA Compliance

POCAMLA keeps moving in one direction. More sectors get pulled in, penalties get heavier, and the bar for what counts as compliant keeps climbing. That trend shows no sign of slowing down, which means the rules businesses are working with today will likely look outdated again before long.

FlexComply, an award-winning, end-to-end compliance solution by FlexM, the leading global fintech conglomerate, gives Kenyan businesses everything they need to stay compliant, from identity verification and due diligence to transaction monitoring and regulatory reporting, so they can stay ahead of POCAMLA compliance rather than scramble to catch up every time it changes.

.png)

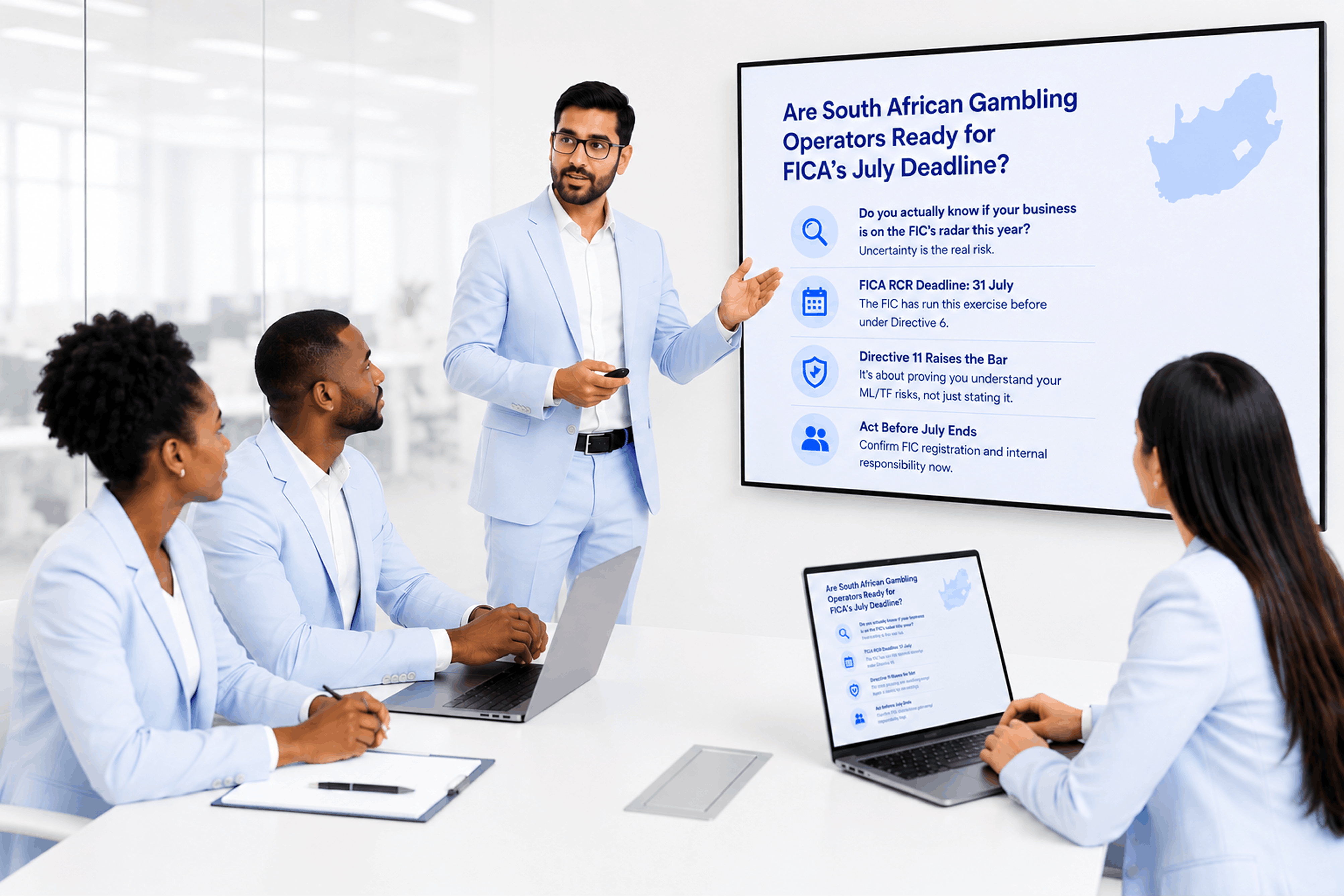

Do you actually know if your business is on the FIC's radar this year?

For a large number of gambling operators in South Africa, the honest answer is uncertain, and that uncertainty is the actual risk, not just an inconvenience. The FICA RCR deadline falling on 31 July isn't new territory for the Financial Intelligence Centre. The regulator ran this exact exercise before, under Directive 6, and institutions that ignored it or assumed it wasn't urgent ended up facing formal notices and sanctions once the FIC followed through.

That history matters because Directive 11 isn't asking for less this time. It's asking accountable institutions, gambling operators included, to prove they understand the money laundering and terrorist financing risk sitting inside their own business, not simply state that they do. If your business hasn't confirmed its FIC registration status, or isn't certain who internally is responsible for this submission, that gap needs closing well before the end of July, not during it.

FIC Directive 11 and the 2026 Risk and Compliance Return

FIC Directive 11 requires specified accountable institutions, gambling operators included, to submit a Risk and Compliance Return 2026 report to the Financial Intelligence Centre. This report asks businesses to self-assess two things: how well they understand their exposure to money laundering, terrorist financing, and proliferation financing, and how effective their actual controls are at managing that exposure.

A written policy sitting untouched in a compliance folder won't hold up here. The FIC isn't asking whether a programme exists on paper, it's asking whether the business can demonstrate that programme is actually working, and that gap between documented and demonstrated is exactly what the RCR is designed to expose.

Here's what the submission actually involves:

- To be submitted electronically through the FIC's goAML platform, not by email or hard copy

- To cover three years of activity, from 1 April 2023 to 31 March 2026, so historical data needs to be on hand, not just current records

- To be filed by 31 July 2026 for non-casino gambling institutions specifically

- Once filed, cannot be edited or withdrawn, which makes internal review before submission essential

Gambling Institutions FICA: Are You an Accountable Institution?

A lot of gambling businesses in South Africa don't realise they fall under FICA until a notice actually lands in their inbox, and by then the runway to prepare properly has already shortened considerably. Under Schedule 1 of the FIC Act, gambling institutions sit as Item 9, which places the entire sector under FICA obligations, covering all four legal forms of gambling recognised under the National Gambling Act, 2004. That means casinos, bingo, betting, and limited payout machines are all in scope, each one licensed by a Provincial Licensing Authority somewhere across South Africa's nine provinces.

The reasoning behind this classification comes down to how the industry actually operates. Cash moves quickly here, and stakes get placed and settled with very little friction between deposit and payout, which is precisely the kind of environment that makes gambling attractive for laundering illicit money. That's why the FIC applies the same level of seriousness to gambling operators as it does to legal practitioners and estate agents, rather than treating the sector as a lower priority.

Size doesn't change any of this either. A single-site bingo hall carries the same gambling institutions FICA status as a bookmaker with dozens of branches across the country. Whether the operation is small or large, the FICA compliance deadline South Africa businesses are racing against this July applies just the same.

Licensed and Compliant Are Not the Same Thing

Running a gambling operation in South Africa means satisfying two regulators with two entirely different mandates, and the complexity sits in managing both properly, not just knowing they exist.

The National Gambling Board handles licensing, through your Provincial Licensing Authority and its Verified Gambling Operators Web Portal. That confirms you're legally entitled to operate. It says nothing about money laundering risk.

The Financial Intelligence Centre asks a different question entirely. Not whether you're licensed, but whether you understand your money laundering, terrorist financing, and proliferation financing risk, and can prove your controls manage it, before the FICA RCR deadline arrives.

Both deserve equal attention. Your licence protects your right to operate, while your standing with the FIC protects you from sanction. That second obligation is exactly what the FICA compliance deadline South Africa has set for this July, and no approval from the NGB covers for it.

Preparing Your goAML RCR Submission

The FICA RCR deadline doesn't leave room for figuring things out as you go. A clean goAML RCR submission depends on groundwork most institutions underestimate until they're already behind on it.

Registration comes first, and it isn't optional:

- A valid FIC Org ID, issued through goAML, is required before the submission option is even available

- Outdated or incomplete registration needs correcting on its own timeline, well ahead of filing

Once registration is confirmed, preparation is what actually determines how smooth the submission goes:

- Review the FIC's sample questionnaire in advance, gambling institutions work from a sector-specific edition, not the generic composite version

- Pull together your Risk Management and Compliance Programme, customer due diligence records, and history of regulatory reports filed with the FIC

- Make sure this covers the full three year reporting period the RCR requires, not just the most recent year

A few rules govern the filing itself. Only a compliance officer, or someone with equivalent authority, can submit, third party providers are not permitted to file on an institution's behalf. And once submitted, the RCR is final, with no way to edit or withdraw it afterward.

What Missing the Deadline Actually Costs You?

Non-compliance under FICA carries formal, financial consequences, and gambling operators weighing whether this deadline is worth prioritising should know exactly what those consequences look like before deciding.

Section 45C of the FIC Act sets out what the FIC can actually do to a non-compliant institution:

- Financial penalties of up to R10 million for a natural person

- Financial penalties of up to R50 million for a legal entity

- Cautions and formal reprimands

- Remedial directives requiring specific corrective action

- Restrictions or suspension of business activities in serious cases

- Public disclosure of the sanction, unless compelling circumstances justify withholding it

Public disclosures are worth sitting with for a moment, because it changes what a sanction actually costs an operator. A financial penalty is a number that gets paid and eventually forgotten. A published sanction is different, it stays visible to banking partners, correspondent institutions, and other regulators long after the fine itself has been settled, and it shapes how those relationships treat the business going forward.

The numbers so far suggest a lot of institutions are still exposed to this risk.

Casinos, along with crypto platforms, trust companies, and credit providers, faced an earlier deadline of June 30th. But by mid-June 2026, the FIC reported a shockingly low compliance rate of just under 12%. As out of over 5,600 registered businesses across these sectors, a mere 655 had actually filed their returns.

Directive 6 already ran this exact process once. The FIC issued formal notices of intention to sanction against institutions that failed to submit, and that enforcement record is the clearest signal available for how seriously the current Directive 11 gambling deadline will be treated. Nothing here is speculative. It's a repeat of a process the regulator has already carried out, with documented consequences for the institutions that didn't take it seriously the first time.

Gambling operators carry a particular exposure here that other sectors don't share as sharply, since the industry already moves large volumes of cash through rapid transactions, exactly the profile the FIC treats as elevated risk. An operator that files late, or not at all, doesn't just sit outside the rules on paper. It gets flagged into precisely the risk category this entire system was designed to identify.

Meeting the FICA Compliance Deadline South Africa

The FICA compliance deadline South Africa has set for gambling operators this year rewards preparation. It penalises delay just as clearly. There's very little middle ground between the two.

Registration needs to be sorted well before July. Sector-specific documentation needs to be gathered. Risk Management and Compliance Programme records need to be in order, not assembled under pressure once the submission window is closing.

FlexM has spent over a decade building compliance infrastructure for regulated and non-regulated entities across the globe, including South Africa, which is what makes FlexComply relevant here. The platform brings risk assessment, transaction monitoring, and regulatory reporting into one system, so operators aren't piecing together evidence from scattered records when a deadline like this one arrives.

Meeting this deadline isn't just about avoiding a sanction. It's what keeps a gambling business operating with the full confidence of its regulator, its banking partners, and the market it serves.

What if your fraud prevention controls are working exactly as designed, and that is precisely the problem?

Across the United States, risk and compliance teams are closing cases, clearing alerts, and reporting fraud losses within acceptable thresholds, while a completely different category of financial crime is scaling invisibly underneath those metrics.

Most AI fraud prevention strategies in use today were built around human fraudsters making human mistakes and leaving human traces. But the dominant fraud threat of 2026 is not human. It is algorithmically generated, behaviorally convincing, and specifically engineered to look clean inside the very systems designed to catch it. Synthetic identity fraud alone is projected to cost US businesses between $30 and $35 billion annually, and it now accounts for up to 80% of all new account fraud, yet represents only 4% of fraud cases by frequency. That gap between frequency and financial impact is exactly what makes it so dangerous and so difficult to act on.

The uncomfortable reality is that AI has not just changed how fraud is committed. It has fundamentally changed what fraud looks like.

AI-Driven Fraud Is Rewriting Financial Crime in the US

For most of the past decade, fraud in the United States followed a recognisable pattern. A stolen credential, a compromised account, a suspicious transaction that triggered an alert. The tools built to catch it were designed around that pattern, and for a long time they worked reasonably well. That era is over.

Fraudsters in 2026 are operating AI systems that run continuously, adapt in real time, and are specifically engineered to exploit the gaps in conventional fraud detection and prevention infrastructure. These are not isolated criminal actors making opportunistic moves. They are organised networks deploying machine learning to manufacture false identities, generate convincing synthetic documents, and automate attacks at a scale that human review cycles simply cannot match.

What this shift looks like in numbers:

- US businesses reported losing 9.8% of annual revenue to fraud in 2025

- AI-enabled fraud losses are projected to reach US$40 billion in US by 2027

These are not numbers that reflect a problem under control. They reflect a problem that has been consistently underestimated because the most damaging fraud category barely registers in case frequency data while quietly driving an outsized share of total financial losses.

Synthetic Identity and Deepfakes: One Industrialised Threat

Generative AI has given fraudsters something they never previously had, which is the ability to manufacture a believable human identity at scale and use it to systematically extract money from financial systems over an extended period of time.

A synthetic identity fraud profile combines real data fragments, typically a legitimate Social Security number paired with a fabricated name, address and contact details, to create a person who does not exist but passes every standard verification check. This identity is then used to open financial accounts, build a credit history through months of normal-looking activity, and steadily increase available credit limits until the fraudster decides the ceiling is high enough. At that point every credit line is maxed simultaneously, the funds are moved and the identity is discarded, leaving no real victim to file a report and no trail meaningful enough to follow.

The one control that historically stood between a synthetic identity and a fully operational account was biometric verification. Deepfake technology has made that control increasingly unreliable:

- Fraud attempts leveraging deepfake content have climbed more than 2,137% over the last three years

- Around 1 in every 5 biometric fraud attempts now involves face swaps or animated selfie manipulation engineered specifically to defeat liveness detection

- Only 13% of companies currently run any anti-deepfake protocols, meaning the vast majority of US businesses are encountering this threat without a specific defense against it

These are not two separate problems requiring two separate responses. They are sequential steps in the same industrialised pipeline, and together they have made AI-driven fraud detection one of the most urgent and least solved challenges in US financial services today.

Detect deepfakes. Block synthetic identities.

Synthetic identities are not just used to access credit. They are used to build the infrastructure through which fraudulent funds move internationally:

- Money mule networks exploit remittance corridors specifically because monitoring across jurisdictions is fragmented

- Each leg of a cross-border transaction obscures the origin of funds further, making the trail progressively harder to follow

- By the time a suspicious pattern surfaces, the money has typically already cleared several intermediary accounts across multiple geographies

The regulatory environment adds further pressure on US businesses managing cross-border flows:

- FinCEN requirements, OFAC sanctions obligations and state-level MSB regulations each carry distinct monitoring and reporting demands

- Businesses handling high transaction volumes across multiple corridors carry significant exposure when these are treated as separate obligations rather than a connected compliance framework

- Fraud monitoring and regulatory compliance handled in silos means organised fraud networks find the gaps before you do

Effective cross-border remittance fraud prevention was never about more tools. It was always about a single connected view.

Why Traditional Fraud Prevention Software Is Failing

The fundamental problem with most fraud prevention software currently in use across the US is not that it is poorly built. It is that it was built for a different threat environment entirely.

The Fraud Detection Gap:

When fraud is specifically designed to look normal, a system built to detect abnormality will consistently miss it. Rule-based transaction monitoring flags anomalies based on predefined patterns. Synthetic identities do not produce anomalies. They produce clean transaction histories, healthy credit scores and behaviours that look entirely legitimate until the moment they do not.

Traditional adverse media screening faces the same structural problem. Keyword-based systems flag anyone mentioned near a negative term regardless of their actual role in the story. A judge presiding over a fraud trial triggers the same alert as the defendant. Hundred articles covering the same incident generate hundred separate alerts. The result is alert fatigue that is not just an operational inconvenience but a genuine compliance risk, because when analysts are buried in noise, the signals that actually matter get missed. AI-driven fraud detection systems have demonstrated the ability to reduce false positives by 65 to 90%, which gives a reasonable indication of how much noise currently exists inside conventional systems.

What Effective AI Fraud Prevention Looks Like in Practice?

Genuine AI fraud prevention in 2026 is not about replacing one set of rules with a smarter set of rules. It is about understanding context, behaviour and risk continuously, across the entire customer lifecycle.

Behavioral intelligence over transaction rules

- Builds a continuous model of how each customer normally operates

- Detects deviations from individual behavioral baselines, not just known fraud patterns

- Catches synthetic identity bust-outs before execution because the behavioral shift preceding them is visible even when the transaction looks routine

Context-aware AI adverse media screening

- Distinguishes between a perpetrator, witness, judicial authority and victim mentioned in the same article

- Clusters related coverage of the same event into a single alert rather than one notification per publication

- Tracks event progression from investigation through to conviction, updating risk profiles dynamically

Perpetual KYC

- Replaces point-in-time onboarding snapshots with continuously updated customer risk profiles

- Triggers reviews when risk signals change rather than waiting for scheduled periodic reviews months away

Real-time fraud monitoring

- Real-time systems prevent substantially higher fraudulent transactions than batch-based processing

- When synthetic identities execute bust-outs across hundreds of accounts simultaneously, the difference between real-time and near-real-time detection is measured in millions of dollars

The businesses best positioned to handle AI-driven fraud are not those with the most tools. They are those with the most integrated tools, where identity verification, screening, behavioral analytics, transaction monitoring, threshold monitoring and regulatory reporting function as a single connected system rather than separate functions with blind spots between them.

Your 2026 Fraud Prevention Checklist

Before your next compliance or risk review, work through these:

- Are your fraud controls built around behavioral signals or purely transaction rules?

- Can your adverse media screening distinguish between a perpetrator and a witness in the same news article?

- Does your cross-border payment monitoring operate as a unified layer or as separate domestic and international functions?

- Are your customer risk profiles updated continuously or only at scheduled review intervals?

- Have you assessed your exposure to deepfake-enabled verification bypass attempts?

- Does your fraud monitoring cover behavioral and device intelligence beyond transaction data alone?

- Can your system detect synthetic identity patterns before a bust-out rather than after?

The Cost of Standing Still Is No Longer Acceptable

The fraud environment facing US businesses in 2026 demands a response that matches the sophistication of the threat. The businesses that navigate this successfully will be those that treat fraud detection and prevention as a unified, AI-powered function rather than a collection of point solutions that communicate only when something has already gone wrong.

FlexM, a leading global fintech conglomerate trusted by over 400+ businesses across the world, has spent over a decade building exactly this kind of integrated infrastructure, purpose-built for the complexity that modern financial crime demands.

The conversations happening this week at New York Fintech Week 2026 in Manhattan, among founders, risk leaders and compliance heads, reflect precisely the urgency that businesses across the US are waking up to. Fraud prevention in an AI-driven world is no longer a back-office compliance exercise. It is a strategic business priority, and the question every US business needs to answer is whether their defenses were built for the version of fraud that already exists today.

Identify gaps across behavior, identity, and real-time risk detection

When Nigeria exited the FATF grey list in October 2025, it was a defining moment for the country's financial system. Years of regulatory reform, institutional coordination and political will had finally paid off. But that exit was never meant to be a finish line. It was a starting point.

The CBN's March 2026 circular has made that unmistakably clear. Every regulated financial institution in Nigeria, from deposit money banks to mobile money operators to payment service providers, must now deploy automated AML solutions that meet new CBN AML requirements 2026. And the first critical deadline is already around the corner: implementation roadmaps must be submitted to the CBN's Compliance Department by June 10, 2026.

For compliance leaders who have spent years navigating manual processes, fragmented systems and growing regulatory expectations, this circular changes the game. It is the most consequential financial crime compliance directive Nigeria has seen in years, and it demands a level of technological readiness that most institutions have not yet achieved.

What Has the CBN Mandated and Who Does It Apply To?

The CBN's March 2026 circular (referenced as BSD/DIR/PUB/LAB/019/002), establishes mandatory CBN baseline standards for AML across the entire regulated financial sector. These standards apply to all financial institutions currently operating under CBN regulation; furthermore, applicants for new licenses must also demonstrate compliance or present a credible implementation plan as part of the authorization process.

The circular introduces three compliance milestones that every institution needs to plan around:

The implementation roadmap is more than a plan; it is a formal regulatory submission that demands absolute precision. To satisfy this requirement, the document must include:

- A current-state assessment and gap analysis to pinpoint specific vulnerabilities.

- The proposed AML solution architecture.

- A phased timeline featuring named milestones and clear owners for every workstream.

- A robust governance and oversight framework.

- A committed resource and budget plan.

This submission requires the highest level of internal accountability, finalized with the signatures of both the CEO and the Chief Compliance Officer.

The CBN is clear that compliance is not a checkbox exercise. The regulator will evaluate demonstrable effectiveness rather than vendor-driven implementation. In practice, simply having a system in place is no longer the benchmark. The regulator now requires proof that the solution delivers measurable results in:

- Detecting complex financial crime patterns.

- Facilitating thorough investigations.

- Maintaining precise, timely reporting.

The 12 Baseline Capabilities That Will Define CBN Compliance 2026

The circular sets out 12 capability areas that every automated AML solution must support. For institutions still relying on manual processes or disconnected point solutions, this list serves as the definitive benchmark against which the CBN will measure readiness.

One requirement in the circular is worth highlighting separately. The CBN has explicitly stated that AML solutions operating solely on transaction data, without effective linkage to customer identity, risk profiles and case histories, will not be considered compliant. Institutions rated High or Above Average risk within their subsector are specifically required to ensure full integration between their AML systems and their KYC/KYB repositories. This effectively ends the era of siloed compliance architecture in Nigeria's financial sector.

Get Your Free Guide

A complete, easy-to-use guide for your gap analysis

Why Is This Circular Different from Previous Nigeria AML Regulations?

Nigerian financial institutions have seen plenty of regulatory updates over the years. So what makes this one stand out?

- Accountability now sits at the top

Compliance is no longer just an institutional responsibility. The circular makes it clear that board members, CEOs, and Chief Compliance Officers can be held personally accountable. A compliance failure is now a direct leadership risk.

- Explainable AI is a regulatory requirement

The CBN has formally introduced AI and machine learning governance into its AML framework. Institutions must deploy automated AML systems, with expectations scaled to their size and risk profile.- Larger institutions are expected to use advanced AI-driven systems

- Smaller institutions can adopt proportionate solutions, but must still meet baseline requirements

- Strict AI governance expectations apply

Any use of AI or ML must include:- Human oversight

- Algorithm transparency and explainability

- Clear reasoning behind every alert generated

- Independent validation at least annually, covering accuracy, drift, fairness, and bias

- FATF Compliance depends on execution

Nigeria’s exit from the FATF grey list was a major milestone. This circular is about sustaining that progress. The CBN is signalling that compliance must be continuous, measurable, and evolving to maintain global credibility.

What Is Actually Holding Institutions Back?

The directive is clear and well-structured. But across the sector, readiness remains a significant concern. What are compliance teams actually up against?

The fraud numbers reinforce the urgency. Nigerian banks lost ₦3.3 billion to fraud in the first quarter of 2025 alone, a 137% increase from ₦1.39 billion in the previous quarter. For institutions still managing financial crime compliance Nigeria requirements through manual and fragmented setups, the risk of falling behind is not theoretical.

Disconnected systems are still common. Identity verification and AML processes often run on separate platforms with limited data sharing. The CBN requires integration across AML systems, core banking, and KYC or KYB data to enable a unified customer view.

The CBN also encourages a unified financial crime setup where AML and fraud systems share risk signals. This means many institutions must rethink how their systems connect and operate.

Too many tools, not enough integration. Nigeria’s RegTech market has expanded, but many solutions are single-purpose. Institutions need to assess vendors based on API capabilities, integration depth, and their ability to support end-to-end compliance needs.

A Step-by-Step CBN Compliance Roadmap to Get Ready Before June 2026

With the June 10 deadline approaching, institutions need a structured approach that meets CBN expectations and supports long-term compliance.

Start with a clear gap analysis. Map your current capabilities against the 12 baseline areas in the circular. Identify what is compliant, where gaps exist, and where systems are misaligned. This forms the foundation for all next steps.

Evaluate system integration. Does your AML case management system connect to your KYC records and customer risk profiles? Does your transaction monitoring engine assess activity within the context of the full customer profile, or does it operate on raw transaction data alone? The CBN has stated clearly that the latter approach is not acceptable.

Prioritise near real-time screening and monitoring. This includes sanctions screening, PEP checks with fuzzy matching, suspicious activity detection across channels, and the ability to block onboarding or transactions instantly when needed. Batch processing is no longer sufficient.

Prepare a Board-authorised implementation roadmap. This must be submitted to the CBN Compliance Department by June 10. Include your gap analysis, solution architecture, phased timeline, governance framework, and sign-off from the CEO and Chief Compliance Officer.

Embed AI governance early. If using AI or ML for risk scoring or detection, document validation processes, explainability standards, and bias testing. The CBN expects outputs that investigators can clearly interpret.

Focus on continuous compliance. The CBN will monitor through ongoing reviews and examinations. Institutions that build for transparency, governance, and continuous improvement will be better positioned than those treating this as a one-time task.

Building Compliance Infrastructure That Outlasts the Deadline

The institutions that will emerge strongest from this transition are those that see the CBN's March 2026 circular not as a regulatory burden but as a catalyst to build compliance infrastructure that delivers lasting value.

FlexM, the leading global fintech conglomerate, offers FlexComply, a 360-degree compliance technology platform designed for exactly this and beyond. As a unified FRAML platform, FlexComply addresses all 12 CBN AML requirements 2026 within a single integrated infrastructure.

Furthermore, FlexComply's AI-powered adverse media screening goes beyond keyword-based matching, using context-aware entity recognition and role-based adversity logic to deliver high-precision alerts with significantly fewer false positives. In a regulatory environment where the CBN now expects explainable AI outputs and continuous monitoring as part of its baseline standards, this capability is no longer optional.

CBN compliance 2026 is not about meeting a single deadline. It is about building the kind of financial crime compliance architecture that earns confidence from regulators, international partners and customers for years to come.

Ready to see where your institution stands against the CBN's 12 baseline requirements?

Get a tailored compliance gap analysis. No sales pitch, just expertise

Money Service Businesses sit at the center of an increasingly complex financial ecosystem. They move value across borders, connect legacy finance with emerging fintech models, and serve millions of customers who rely on fast, compliant and reliable services. But as the sector expands, so do its operational and regulatory vulnerabilities. Even well-established MSBs are finding that growth exposes gaps their legacy systems cannot absorb — a pattern consistently highlighted by leading global fintech conglomerates like FlexM, whose modular platform architecture is built specifically for MSB scalability. In this environment, choosing a scalable Money Service Business platform has become a structural, not optional, decision.

The Industry Has Outgrown Its Traditional Infrastructure

Money Service Businesses now operate within one of the fastest-expanding and most complex financial environments in the world. The scale of value moving across borders has fundamentally shifted. The global cross-border payments landscape is projected to reach US $290 trillion by 2030, signalling not only rapid expansion but also an urgent need for more resilient, intelligent infrastructures capable of supporting such unprecedented flows.

At the same time, the global remittance market — a core operational channel for MSBs — is expected to reach US $744.8 billion in 2025. This surge highlights just how central MSBs have become to cross-border value movement, financial inclusion, and alternative financial rails.

Yet despite this scale, MSBs often operate on outdated, fragmented systems built for a different era. Manual onboarding, spreadsheet-driven reconciliations, disconnected AML tools, and channel-specific workflows all create bottlenecks that compound as the business grows. A modern money service business software resolves these limitations by creating a unified ecosystem where customer onboarding, risk scoring, monitoring, and reporting operate cohesively rather than in silos.

Regulation Has Entered a New Phase — and Money Service Business Platform Are on the Front Line

Compliance is no longer episodic; it is continuous.

The most significant example of this shift came in October 2025, when Canada introduced sweeping AML reforms that tighten MSB registration, strengthen sanctions-reporting requirements, and elevate expectations for transaction traceability and governance oversight. These changes signal an international trend: regulators expect MSBs to demonstrate control, transparency, and auditability at the same level as major financial institutions.

This rise in scrutiny makes a scalable MSB compliance platform indispensable. Instead of retrofitting new rules into legacy processes, MSBs require systems that adapt in real time — recalibrating workflows, updating risk logic, recording audit trails, and supporting ongoing monitoring automatically. FlexM’s modular compliance stack, for example, enables MSBs to adjust rapidly to regulatory shifts without operational disruption.

How a Unified MSB management system Reduces Operational Risk

While regulatory pressure is highly visible, operational strain often becomes the hidden obstacle that prevents MSBs from scaling. As MSBs add new corridors, payout partners, digital channels, agent networks, and customer types, their internal complexity grows exponentially.

This increased complexity typically manifests as:

- inconsistent onboarding decisions

- duplicated customer records across systems

- slow case resolution due to manual reviews

- siloed data resulting in incomplete risk views

- rising operational cost as teams expand linearly with volume

A scalable MSB management system alleviates these issues by consolidating data, automating repetitive workflows, standardizing decision logic, and giving compliance and operations teams a unified real-time view of customer and transaction activity. This reduces cost-to-serve, lowers error rates, and allows MSBs to expand sustainably.

Customer Experience Has Become the Real Test of Modern money service business software

Modern MSB customers expect:

- fast, seamless onboarding

- real-time transaction visibility

- consistent decisioning

- predictable turnaround times

- omnichannel continuity

Whether these customers are individuals, SMEs, marketplaces, or digital platforms, they expect immediacy and clarity — expectations that strain fragmented systems.

A unified money service business software ensures that customer journeys remain consistent even under heavy transaction loads. FlexM’s customer-centric architecture demonstrates how MSBs can maintain service standards while supporting complex multi-corridor, multi-partner environments.

Why Scalability Defines the Next Generation of MSB Leaders

For MSBs, scalability means far more than handling additional volume. It means:

- Regulatory scalability: adapts to new rules, jurisdictions, and reporting structures without painful system rebuilds.

- Operational scalability: workflows remain stable and efficient as activity multiplies.

- Risk scalability: monitoring improves with scale, rather than degrading under pressure.

- Customer scalability: experience quality remains consistent across channels and growth cycles.

- Technology scalability: infrastructure remains reliable during peak loads and expansion phases.

This is the type of scalability required to survive the next decade of regulatory and competitive transformation.

Scalable Money Service Business Platform: The New Competitive Edge

The MSB industry is entering its defining period. Transaction volumes are rising, compliance expectations are intensifying, and customer journeys are becoming more digital and demanding. A scalable Money Service Business platform is no longer an optional upgrade. It is the backbone of MSBs that intend not only to grow, but to lead in a sector where resilience, adaptability, and compliance readiness define long-term success.

FlexM’s modular ecosystem — both compliance, and remittance — gives MSBs a single, integrated foundation built for real-world scale. Discover how your MSB can modernize with confidence: visit flexm.com to learn more.

Where We Made the Difference

The solution was devised as not only a way to embrace digital but also to create a unique model to offer cashback at offline merchants. This enabled the offline retailers to match their online shopping counterparts in creating customer loyalty by integrating proven contactless solutions.

.png)

The Agrani Remit app is an excellent example of how digital innovation helped the Bangladeshis working in Singapore to digitally and conveniently remit money, back to their family members safely…

FlexM, one of our collaborative partners, played a crucial role in conceptualizing the solution (FlexM's Compliance Solution). Their continued support throughout this transition has been invaluable. We are grateful for FlexM's significant contribution to the solution and their unwavering support as we navigate this transition.

FlexM offers invaluable (RegTech) services for monitoring our card transactions and reporting to the RBI. Their expertise and commitment to excellence have significantly enhanced our compliance and risk management processes.